Technical Analysis in a negative world: Who pays who?

Once upon a time life was easy. If you were a ‘good’ person you saved money, deposited at a bank that you trusted, it would earn interest and then, with a bit of luck, you could buy the big-ticket item you had your eye on. That was then; today we are learning that zero is no longer the lower boundary.

Commodity traders have always understood that markets often behave differently at bottoms than at tops. Because numbers are smaller, the maths is different and percentage moves are bigger but nominal ones perhaps not worth stooping for. Volume dries up and the business might become unviable – hence the exodus from the bullion market in the 1990’s, for example.

Traders in penny stocks also favour these precisely because of their small digits. Pick a good-un and it’s possible to flip it quickly for double, three times or ten times the purchase price. If it goes pear-shaped, your downside is small and a known quantity.

But what happens when your bank wants to charge interest on your cash? Currently the case with central banks in the Eurozone, Denmark, Sweden and Switzerland. Like Greeks, one is probably tempted to withdraw it and stash it under the mattress. For corporates, this is not an option.

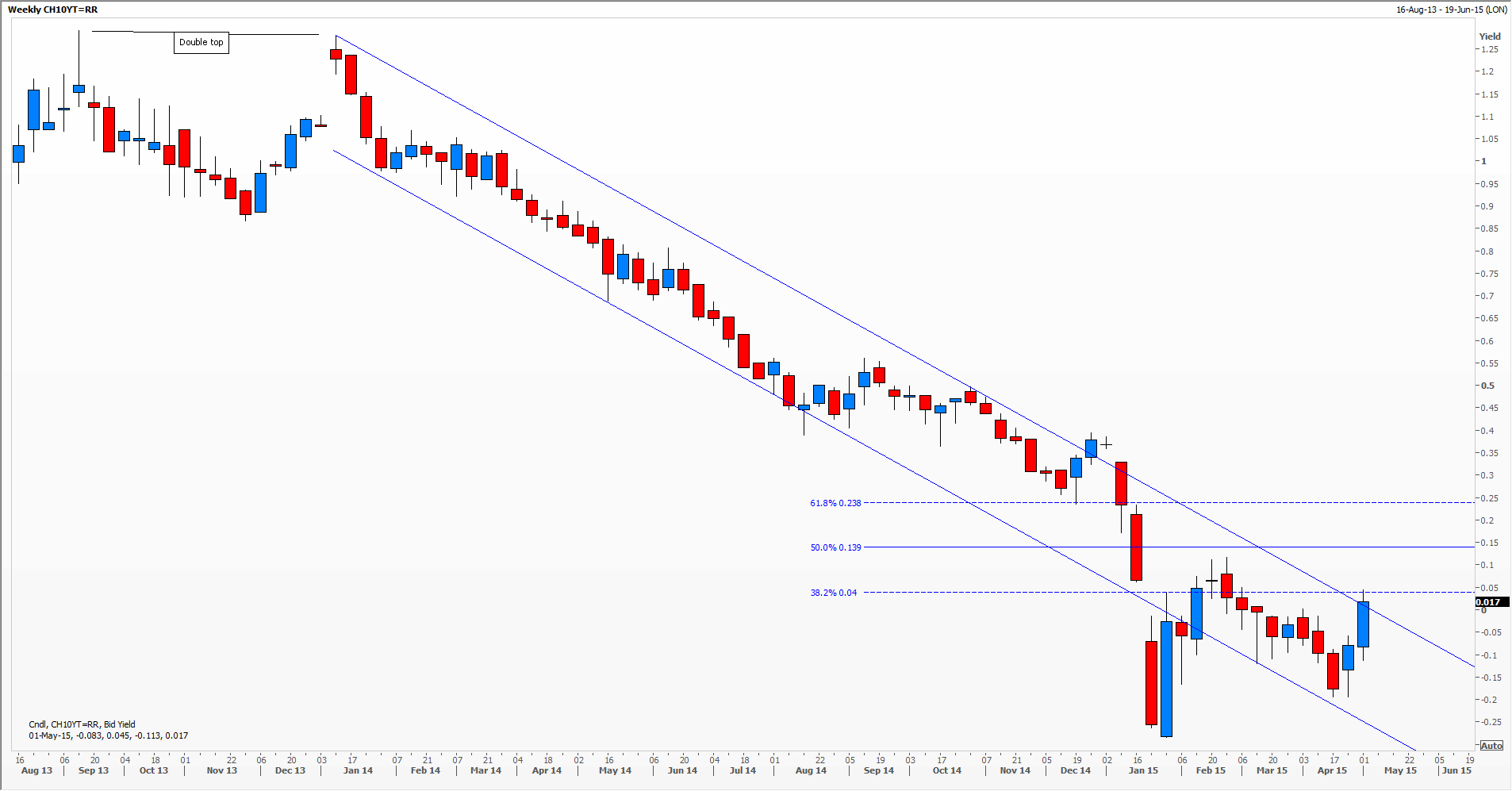

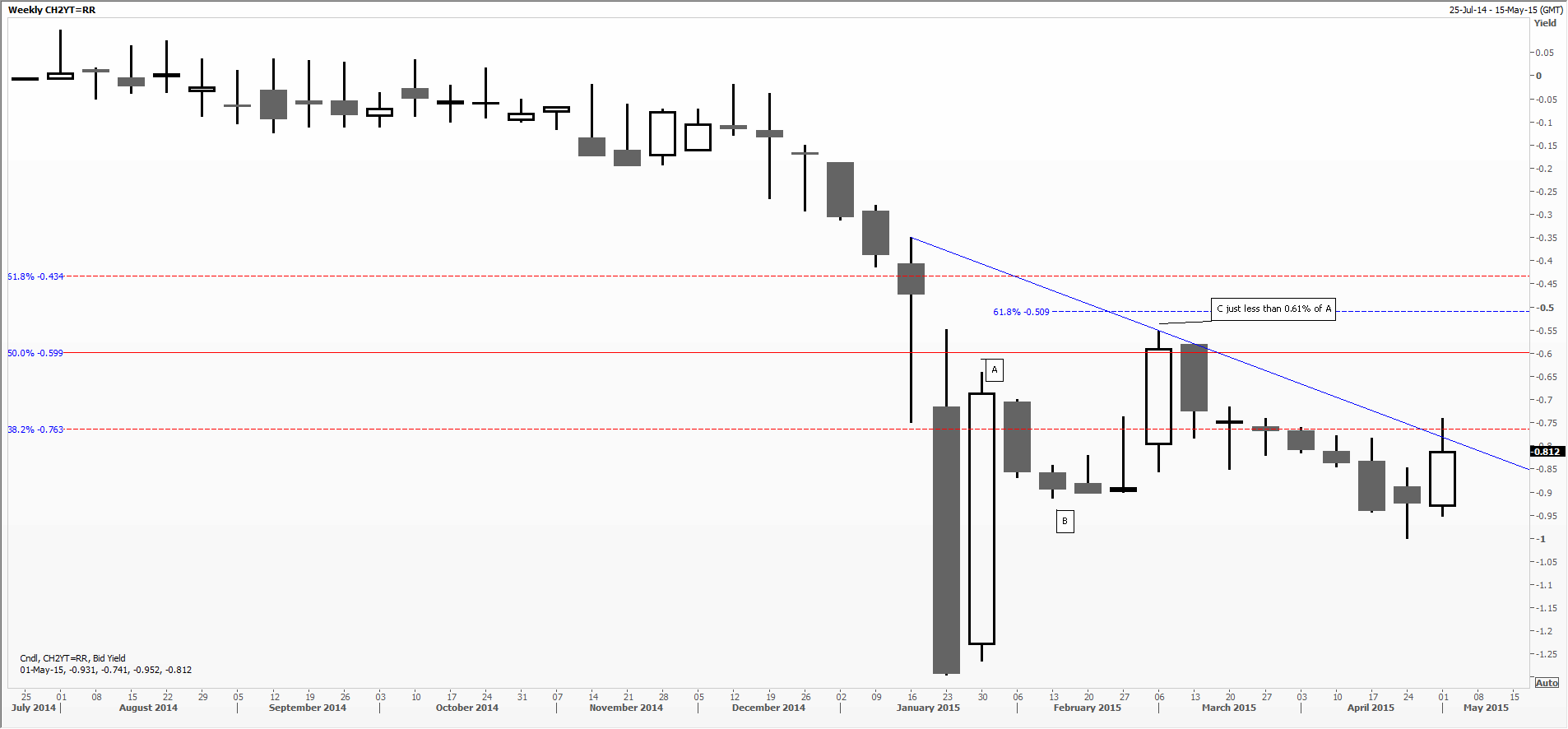

Can charts help? We have attached ones of benchmark yields on Swiss two and ten-year sovereign debt, trading at minus 81 and zero respectively. I think you will agree that both display no obvious signs of stress or outlandish moves, and for the moment are behaving with classic patterns and swings. Two-year building towards a slump over Christmas and New Year, the clear-out was quickly reversed a week later and then an uneasy A, B, C type correction mapped. It tested trend line resistance this week and looks to have stalled at the 38% Fibonacci retracement. Ten-year yields are clearly back inside a trend channel that has dominated since January 2014, also stalling at the 38% level.

Both suggest that Technical Analysis can cope with the highly unusual, which is more than can be said for other analysts who throw up their hands claiming ‘uncharted territory’.

Charts courtesy of Reuters.

Tags: bonds, Europe, interest rates, money, Negative Yields

The views and opinions expressed on the STA’s blog do not necessarily represent those of the Society of Technical Analysts (the “STA”), or of any officer, director or member of the STA. The STA makes no representations as to the accuracy, completeness, or reliability of any information on the blog or found by following any link on blog, and none of the STA, STA Administrative Services or any current or past executive board members are liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. None of the information on the STA’s blog constitutes investment advice.

Latest Comments