Central bankers and their currencies: Too reliant on received wisdom

While teenage climate activist Greta Thunberg is only half-way across the North Atlantic Ocean in her seriously carbon-neutral sailing yacht, central bankers from all over the world flew in yesterday – many in private jets – to Jackson Hole, Wyoming’s (JAC) commercial airport, the only US one inside a National Park; the closest international airport is in Salt Lake City, Utah.

The annual symposium for bankers and top bods in finance, there will be speeches galore and time to discuss informally current trends and preoccupations keeping them awake at night. The Sino-US trade spat for starters, the potential for a global economic slowdown, how to deal with ultra-low and negative interest rates. The list is long and issues pressing.

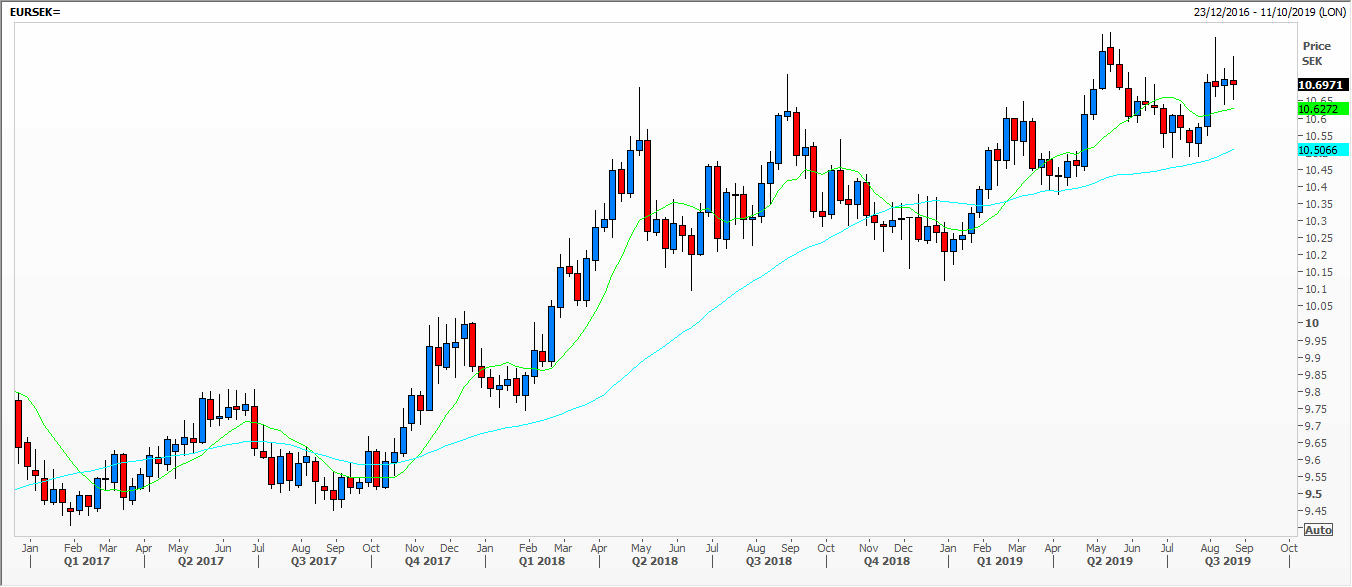

Swedish people have seen a 33 per cent cut in the value of their krona since 2012 (and is one of this year’s worst performing currencies), blaming it on the Sveriges Riksbank’s long-held negative policy rate. Looking at the chart, you can see a slightly erratic rally in the value of the euro against the krona, backing up popular opinion and conventional theories of the effect of interest rates on FX.

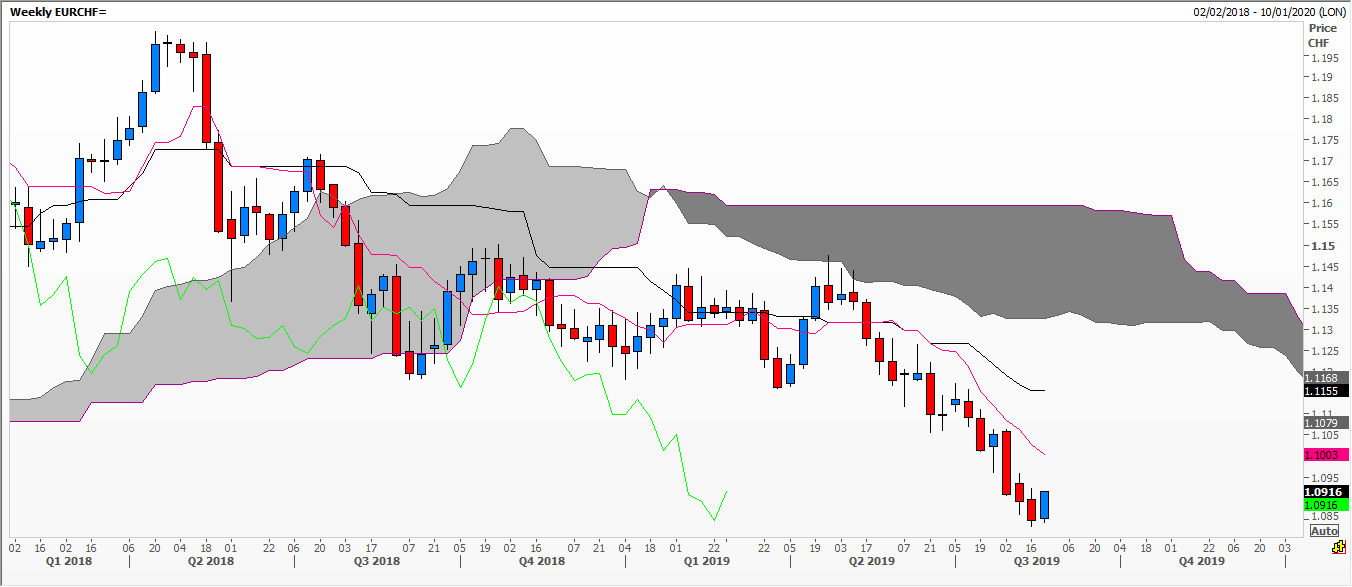

The second chart is of the Swiss franc against the euro, where the Swiss National Bank has spent vast fortunes to prevent their currency from getting so strong that it affects their open economy and exports. As part of the tool kit they too have a key interest rate set at a negative 75 basis points – which will now be levied by some commercial banks on the deposits of wealthy customers. The trend is still clearly intact.

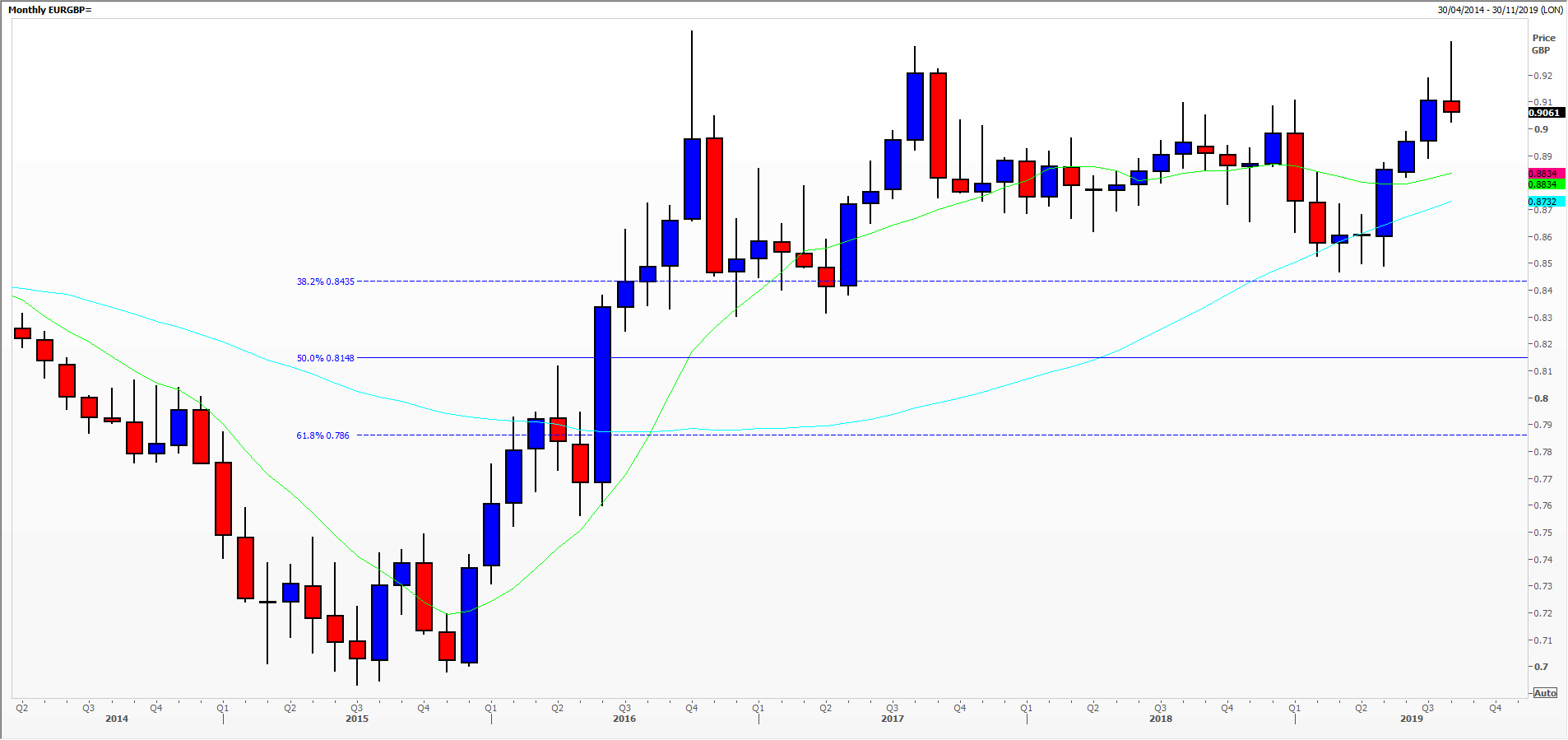

Over in Britain the Bank of England’s Bank Rate is plus 75 basis points while the ECB’s key rate is set at minus 40 basis points – and could go lower still. Nevertheless, courtesy of the Brexit referendum sterling has weakened from just 70 pence per euro in 2015 to a high just over 93. So, you see, interest rate differentials sometimes work and sometimes they don’t. Pretty useless as a policy tool, I’d say.

EURSEK

EURCHF

EURGBP

The views and opinions expressed on the STA’s blog do not necessarily represent those of the Society of Technical Analysts (the “STA”), or of any officer, director or member of the STA. The STA makes no representations as to the accuracy, completeness, or reliability of any information on the blog or found by following any link on blog, and none of the STA, STA Administrative Services or any current or past executive board members are liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. None of the information on the STA’s blog constitutes investment advice.

Latest Comments